3D Secure (3DS)

Integrate 3D Secure authentication in Bamboo using external or Bamboo-managed flows. Compare integration options and learn how to include 3DS data in your purchase requests.

What is 3D Secure?

3D Secure (3DS) is a cardholder authentication protocol designed to add an additional layer of security to online card transactions. It enables issuers to verify payer identity during checkout, reducing fraud in card-not-present (CNP) environments.

When authentication is required, the issuer evaluates the transaction and may request additional verification from the payer (OTP, biometric, push approval, or other challenge).

Why use 3D Secure?

Implementing 3DS offers several advantages:

Adds an authentication checkpoint that reduces unauthorized transactions

For certain schemes and regions, successful 3DS authentication may shift chargeback liability to the issuer.

Required for Strong Customer Authentication (SCA) under PSD2 and other regulatory frameworks.

Supports frictionless flows, meaning many transactions authenticate without visible user interaction

Issuers can authenticate silently when the transaction is considered low risk

3D Secure 2 (3DS2)

3DS2 introduces mobile-first flows, richer data exchange, frictionless authentication, and improved issuer decisioning.

Authentication may occur without a challenge, improving conversion rates

Optimized for mobile web and native applications

Enables OTP, biometrics, and issuer app push approvals.

Merchants can provide contextual data to improve issuer risk evaluation.

Supports 3DS versions 2.0–2.2 with fallback to previous versions when required.

3DS2 improves both security and payer experience through enhanced authentication and risk-based processing

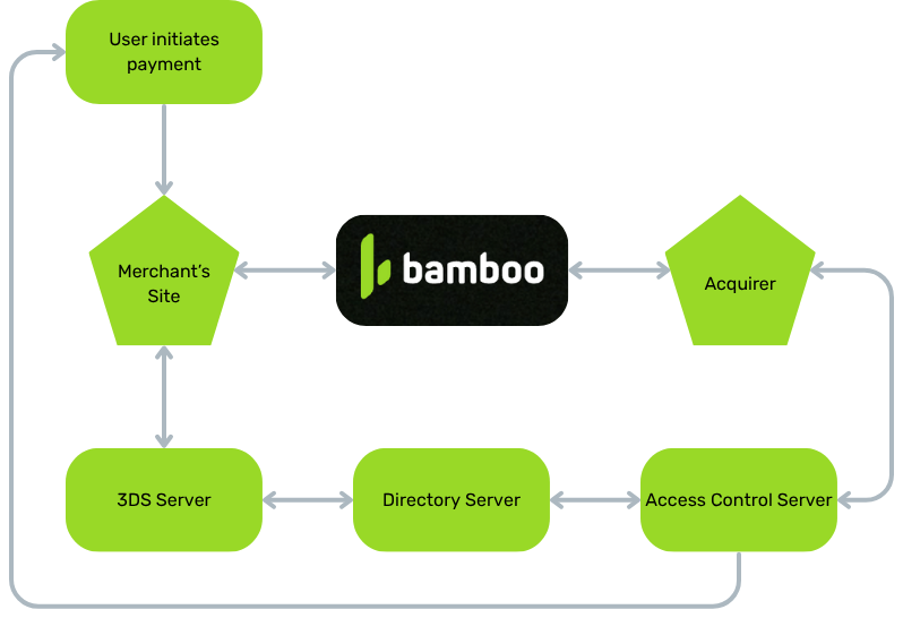

How the 3D Secure Process Works

The 3D Secure (3DS) process relies on several components that work together to verify the cardholder’s identity and enhance transaction security.

1. 3DS Server

The process starts with the 3DS Server, which manages the authentication request on behalf of the merchant.

It gathers relevant information about the transaction and the cardholder and securely prepares the data needed to initiate the 3DS process.

2. Directory Server (DS)

The Directory Server routes the authentication request to the correct Access Control Server (ACS).

It ensures the request reaches the issuer’s domain securely.

3. Access Control Server (ACS)

The ACS is the issuer’s authentication domain. It evaluates the transaction’s risk and decides whether to approve it silently or issue a challenge for further verification.

4. Challenge & Verification

If a challenge is triggered, the cardholder is prompted to verify their identity — e.g., with an OTP, biometric check, or push notification. If successful, the transaction continues. Otherwise, it is declined.

5. Finalization

Once the ACS returns a decision (either frictionless approval or post-challenge confirmation) the result is relayed back. The transaction is either completed or rejected accordingly.

Integration Options

Bamboo supports two methods for integrating 3D Secure authentication. External authentication is currently available. Bamboo-managed flows will be available soon

Updated 8 months ago